As employees and teams contemplate ways to save the Agency money with the Center’s newly introduced “BHAG,” a big hairy audacious goal of having a cost savings or cost avoidance of $20M by fiscal year 2020, a list of guidelines have been created.

Soft Savings / Cost Avoidance: Indirect savings improves capacity, regains process controls, or avoids planned spending through improvements or efficiencies. This type of savings or avoidance removes the expenses from a specific process for which the savings dollar does not affect budget levels.

Some examples of soft savings include:

Hard Savings / Cost Savings: The removal of expenses from a specific process is classified as hard savings or cost savings. These are savings that provide direct improvement to the bottom line. These cost savings may or may not be recognized in budgetary levels. The savings may be redirected to create more buying power for the customer.

Some examples of hard savings include:

In some instances, the identification of an improvement as either a cost savings or cost avoidance may be difficult to determine. Organizations should try to be consistent, to the maximumextent possible, in the application of definitions.

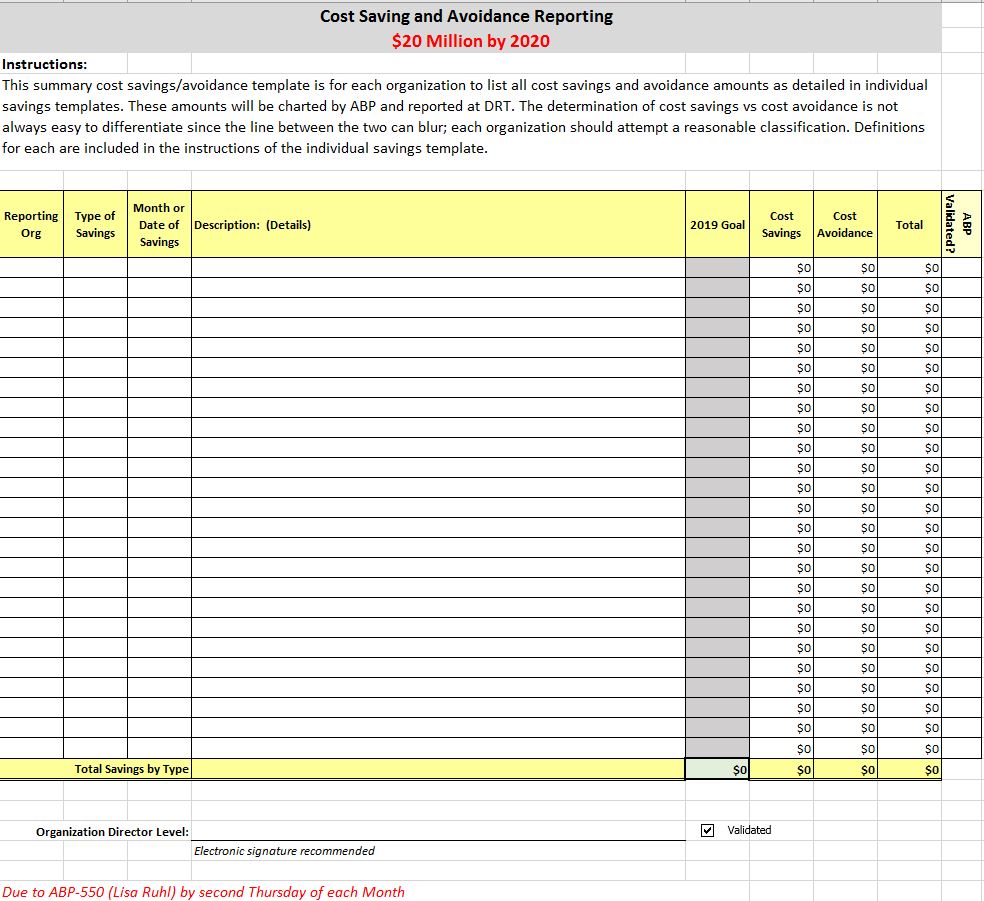

Validation:

Validation will consist of reviewing line items for practicality and accuracy. First level validation is performed on each individual saving worksheet, by the organization’s financial representative. Second level validation is performed by the organization’s director (AMA-1, AMK-1, and AMP-1) on summary of saving worksheet. Please apply electronic signatures using PIV card.

Third level validation will be performed by the Office of Budget and Performance for AMC (ABP-550).

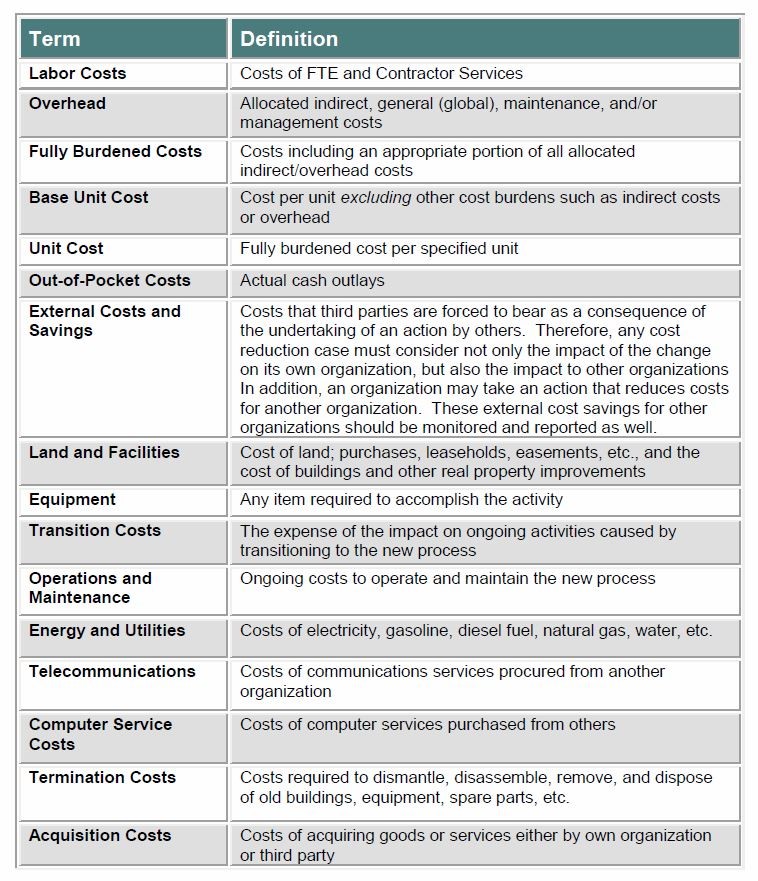

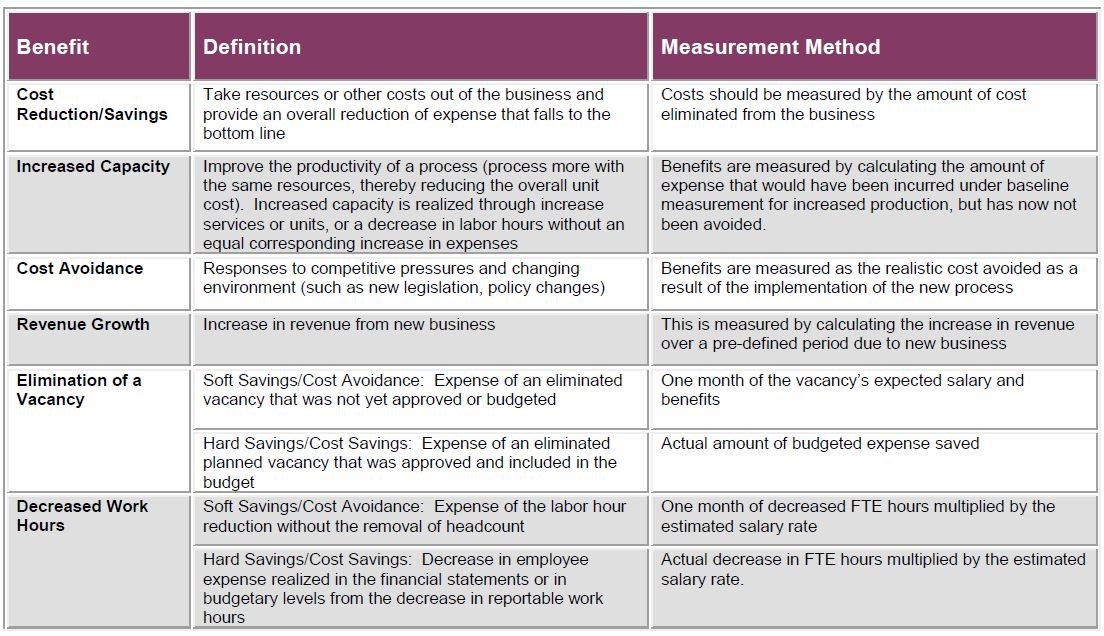

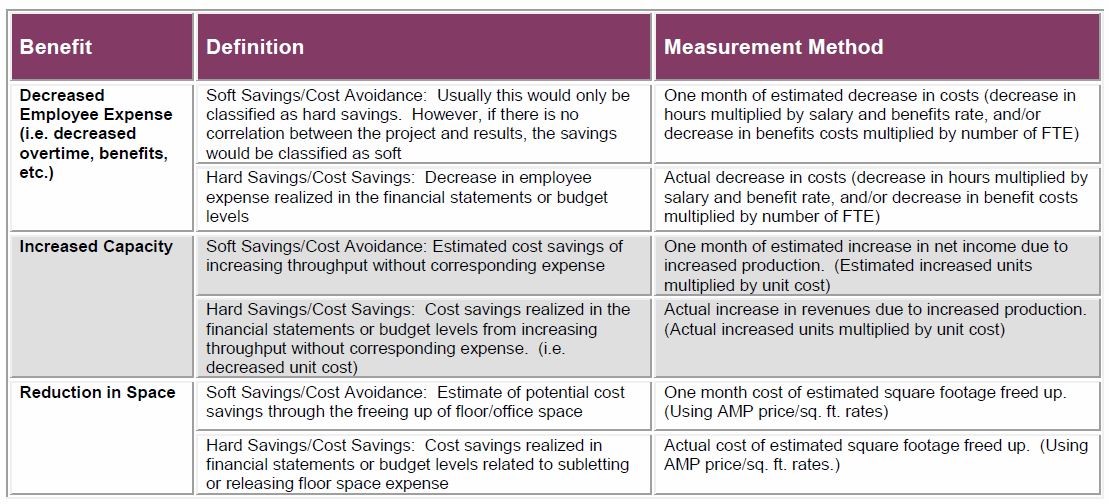

Listed below are examples of savings categories, definitions, samples of hard and soft savings, and suggested methods of measurement.